It’s the start of Fashion Month—the pinnacle of luxury, where fashion houses invest millions into runway shows to reinforce their brand identity. But how does this impact their beauty divisions?

This episode explores the role of beauty within luxury fashion houses. Why do these brands expand into beauty? How does the business model differ from fashion, and how do they compete in an increasingly saturated beauty market? From shifting ownership structures to evolving retail strategies, we break down how luxury fashion brands can compete in beauty in 2025.

The Business of Luxury Beauty

Luxury fashion houses face a delicate balance between accessibility and exclusivity. Beauty offers customers a more accessible entry into a brand while maintaining enough distinction in positioning to uphold the prestige of its fashion offering.

Licensing

Historically, luxury beauty operated via licensing agreements—fashion houses partnered with beauty conglomerates like Coty, L’Oréal, and Puig to handle production and distribution in exchange for a profit share. Coty alone manages a huge luxury portfolio.

As beauty gains global traction, luxury houses are re-evaluating their strategies. LVMH saw beauty sales reach $8.8B, yet this pales in comparison to its $45B in fashion and leather goods. Luxury beauty’s small market share (4% of retail sales in 2023) boasts the highest compound annual growth rate at 9%. However, luxury fashion houses aren't experiencing this growth, as their licensees are underperforming. Coty's stock, for example, has dropped 44% in the past year, and they're not the only ones facing challenges.

Shifting Strategies

Brands are reclaiming control over their beauty businesses:

Ending Licensing Agreements: Dolce & Gabbana has taken their beauty divisions in-house for greater control. Prada and Miu Miu switched from Puig to L’Oréal to expand into makeup.

Building Internal Beauty Divisions: Kering launched its own in-house beauty department in 2023, possibly signaling a future split from Coty for Gucci.

Acquiring Fashion Houses: Estée Lauder acquired Tom Ford for $2.8B to maintain ownership over the beauty business. Similarly, Puig acquired Dries Van Noten.

Luxury beauty is evolving from a licensing model to in-house control, reflecting its increasing importance in the luxury market. Fashion houses are realising that beauty isn't just a sideline—it's a lucrative, growing business.

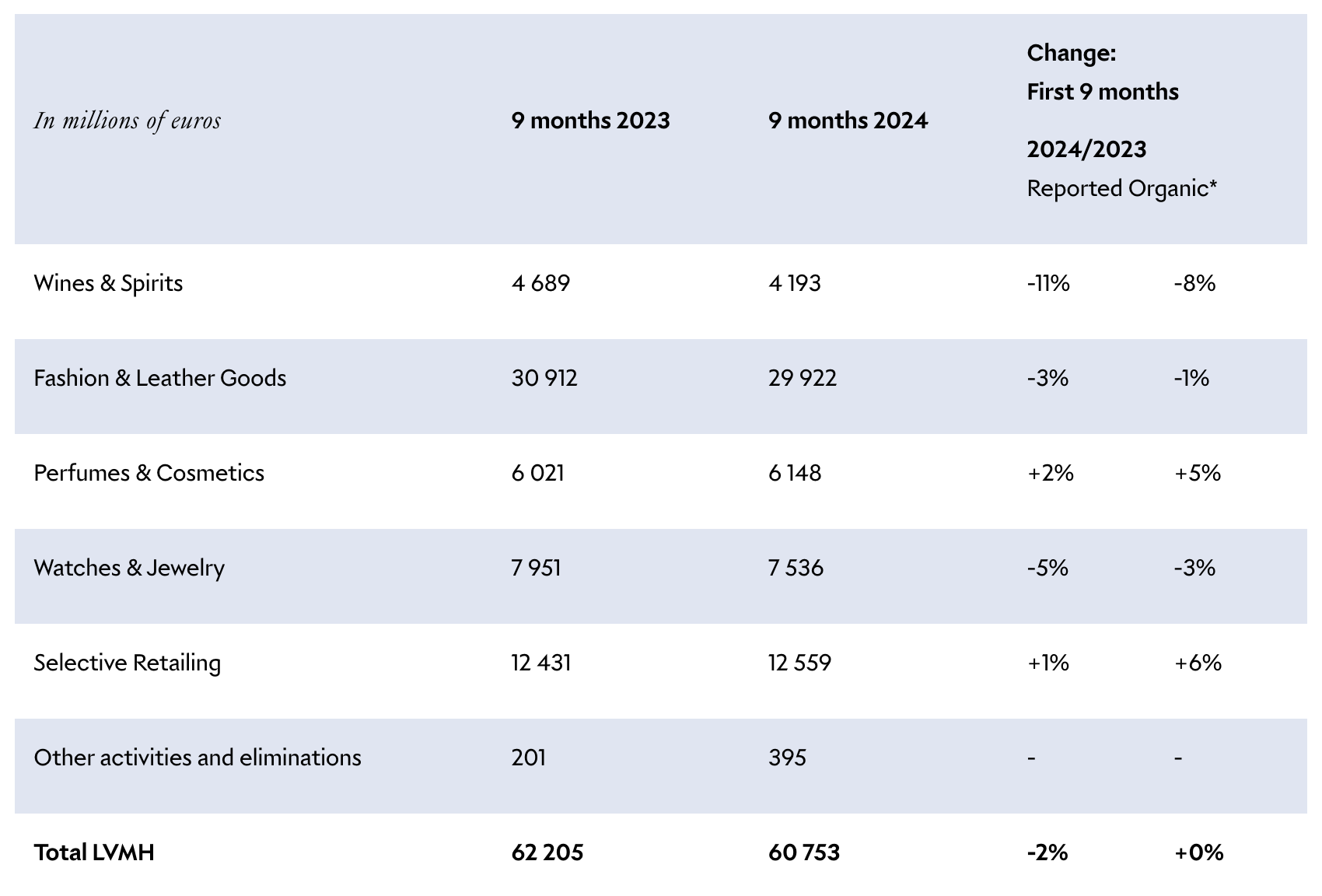

LVMH’s October 2024 report shows why, perfumes and cosmetics grew +5%, while fashion (-1%), watches and jewelry (-3%), and wine and spirits (-8%) declined. The only other category with growth was selective retailing (+6%), driven by Sephora. As brands take beauty in-house, it's clear that luxury’s future isn’t just in fashion—it’s in beauty.

Retail

With luxury fashion houses rarely owning their beauty divisions, a disconnect emerges between fashion and beauty strategies—most evident in retail distribution. Historically, profitability in luxury beauty required mass distribution, leading to 15,000–20,000 retail touchpoints compared to fashion’s 400. Yet, as former Estée Lauder executive John Demsey told WWD about the success of Tom Ford Beauty: “The distribution is really tight.” A level of control few luxury beauty brands can claim.

The Scale of Luxury Beauty

Luxury beauty operates on a different model than fashion. Despite having higher profit margins, its lower price points force it to rely on volume sales. This has historically justified mass distribution, making luxury beauty accessible in department stores, duty-free outlets, and even mass-market retailers like Amazon and Chemist Warehouse.

But this strategy is facing challenges. The rise of prestige beauty—selectively distributed brands like Le Labo, Maison Margiela, and Dr. Barbara Sturm—is shifting consumer expectations. The luxury brand name is no longer enough to sell a beauty product.

Travel Retail: A Controlled Luxury Experience

Travel retail, specifically in airports, has become a major growth channel for luxury beauty. The sector is projected to surpass $117 billion in global sales by 2030, growing at nearly +10% annually.

Luxury brands benefit from travel retail due to:

High Foot Traffic: Major airports see millions of travelers per month (JFK: 5.2M, Heathrow: 8M), surpassing traditional malls.

Forced Dwell Time: Passengers spend extended periods in duty-free zones, increasing purchase likelihood.

I believe the primary reason luxury brands are focusing on retail is the curated environment. Unlike traditional retail, travel retail gives luxury brands control over their surroundings, ensuring they are placed alongside other premium brands.

Here’s some footage I captured at Sydney International which helps visualise this bizarre retail experience. It’s like a department store if it was better maintained and only luxury brands were allowed to open stores.

Travel retail is becoming a key strategy for luxury beauty brands, offering exclusivity and a curated shopping experience akin to high-end fashion. It allows brands to link their beauty products to premium travel experiences, similar to how retailers like Sephora and Mecca curate their beauty environments to evoke associations with prestige brands.

While post-COVID uncertainties raised doubts for travel retail, the sector is poised for growth, with Airports Council International forecasting a 10% rise in foot traffic in 2024. As transatlantic travel matures, emerging markets like India and the Middle East present significant opportunities for luxury beauty brands looking to expand, with Europe and North America currently dominating the sector.

To succeed, luxury brands need to build awareness ahead of time through effective storytelling and strategic positioning so consumers are primed to buy when they encounter products in duty-free stores.

Marketing

Before diving into luxury marketing strategies, it’s important to assess if they’re actually working. By using Reddit’s API to analyse 1,000 comments across both fashion and beauty brands Chanel, Gucci, Dior, and YSL we can gauge the perception of these brands.

Key Findings:

Chanel Beauty: 9% more positive sentiment than Chanel Fashion.

Gucci Beauty: 5% more positive sentiment than Gucci Fashion.

Dior & YSL Beauty: Slightly less positive sentiment than their fashion lines.

Gucci Fashion had the most negative sentiment switch (18%).

On the whole, each of these brands is surprisingly comparable.

The old luxury beauty brands are established but lack excitement, while younger brands like Bottega Veneta and Loewe are redefining luxury beauty. These brands focus on design, with products like Loewe’s AU$270 candles and Bottega Veneta’s AU$700 perfumes being as much about home decor and design as they are about fragrance.

Key Takeaways:

The Need for Creativity: The advantage luxury brands have over prestige brands is their ability to push creative boundaries. To stand out in an oversaturated market, design and creativity will be the key.

Luxury’s Advantage: Fashion Week has long been an essential marketing tool for luxury fashion, providing a platform to showcase creativity. By extending the creativity of runways, couture, and ready-to-wear into beauty, luxury beauty brands can shift away from feeling like a cash grab and instead emphasize their fashion house's innovation and artistry.

That concludes this week’s episode. If you enjoyed this post or the podcast, be sure to give it a like and share it with a friend! Thanks for tuning in, and I’ll see you next time!

Share this post